Categories

- Case Study (12)

- Industrial Building (4)

- ESG (24)

- Fit-Out (3)

- News (56)

- Interior Architecture (11)

- Architecture (22)

- Office (45)

- Studio Alliance (24)

- History (2)

- Design (20)

- Technology (13)

- Artificial Intelligence (AI) (4)

CBRE’nin yayımladığı 2025 Avrupa Gayrimenkul Piyasası Yıl Ortası Raporu, yıl başındaki öngörülerin hangi yönde evrildiğini ve ikinci yarıda hangi fırsatların öne çıkacağını net bir şekilde ortaya koyuyor. Düşen faizler, artan uluslararası yatırım ilgisi ve sektörel farklılaşmalar, 2025’in geri kalanına umut verici bir tablo çiziyor.

Consumer-driven growth continues in Europe. The ECB has cut interest rates four times this year, with another cut expected towards the end of the year. The BoE is also expected to cut rates three times, bringing them down to 3.5%.

While rising real wages, low unemployment and strong consumption support the market, political risks such as the US's new tariffs are on investors' radar.

In 2025, international capital, particularly US-based private equity funds, returned to Europe.

Avrupa genelinde konut arzı talebi karşılayamıyor. İnşaat izinleri hedefin %64’ünde kaldı.

Yüksek göç, artan talep ve yetersiz arz, büyük şehirlerde kiraların 2026–2030 arasında yıllık ortalama %3,3 artmasına yol açacak. İrlanda ve İngiltere gibi ülkeler, katı kira kontrolleri yerine inşaatı teşvik eden politikalara yöneliyor.

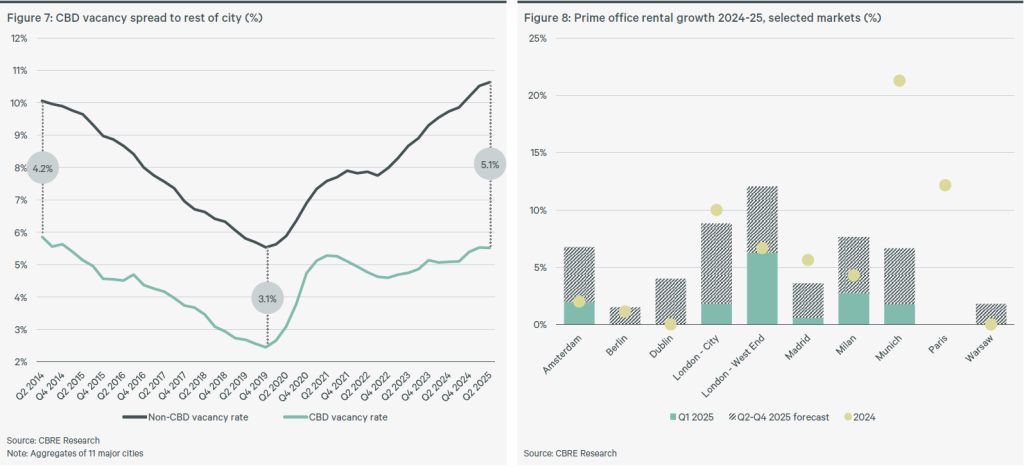

Although the vacancy rate has risen above 5%, it is expected to stabilise by the end of the year. High-standard, efficiency-enhancing warehouses are the focus of investors.

The gap in rents and occupancy rates between city centres (CBDs) and surrounding areas is widening. Double-digit rent increases are forecast for 2025 in cities such as London's West End, Rome and Frankfurt.

Retail parks lead the way with a 4% rent increase. Demand is strong in high street and prime shopping centres, with low vacancy rates. Consumer confidence fluctuates, but spending remains resilient.

The influx of tourists from the US and other global markets is supporting hotel occupancy and prices. RevPAR growth is in the range of 2–5 per cent. The slowdown in new hotel investments is putting upward pressure on room rates.

2025’te Avrupa’da 854 MW ile rekor kiralama hacmi bekleniyor. FLAPD piyasalarında boşluk oranı %6’nın altına inecek. Güç arzı kısıtı ve yapım maliyetleri, kiraları bazı pazarlarda %10’dan fazla artırıyor.

Avrupa’daki kredi verenlerin %71’i, sürdürülebilirlik kriterlerini karşılamayan gayrimenkullere kredi vermiyor. Retrofitting projeleri yatırım stratejilerinin merkezinde. AB’nin yeni raporlama yükümlülükleri, yatırımcılar için hem zorluk hem de fırsat yaratıyor.

In summary: In the second half of 2025, the low interest rate environment, strong international capital interest and sectoral opportunities present significant potential for investors. However, supply shortages, political uncertainties and sustainability criteria require strategic planning.